The recent performance of Australian businesses is failing to meet their own expectations as a continuation of below-trend growth in the economy begins to impact reported activity this year.

The recent performance of Australian businesses is failing to meet their own expectations as a continuation of below-trend growth in the economy begins to impact reported activity this year.

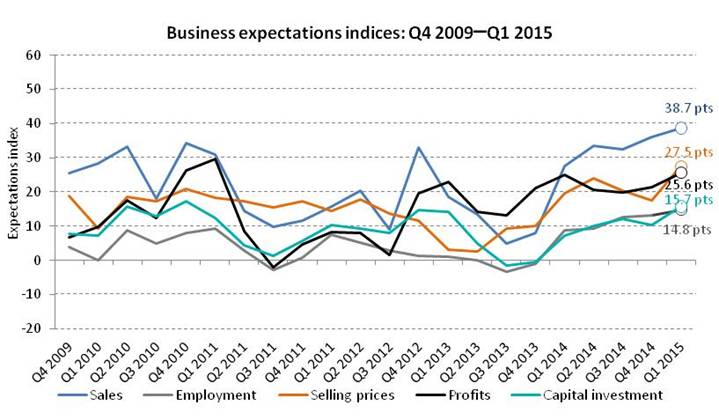

According to Dun & Bradstreet’s Business Expectations Survey, sales and earnings in particular are falling further behind the three-month projections being made by businesses.

Compared to initial expectations, the number of businesses that achieved an increase in sales during the third quarter fell from 43 per cent to 38 per cent. At the same time, the proportion of businesses that reported reduced sales was 20 per cent; more than the 11 per cent that had initially forecast weaker activity. These responses have moved the actual sales index to 18.3 points for the September quarter, short of the expectations index of 32.5 points. Upbeat sales forecasts through to the first quarter of next year have lifted the index further, to 38.7 points.

A similar trend has developed in the profits performance of businesses this year. D&B’s survey has found that, while 35 per cent of businesses had expected higher earnings in the September quarter, only 27 per cent delivered. Additionally, 19 per cent of firms experienced a decline in their profits compared to the 15 per cent that had initially forecast a drop in earnings. The Q1 2015 outlook for profits is 25.6 points, marginally higher than the 25.0 points forecast at the same time last year.

A similar trend has developed in the profits performance of businesses this year. D&B’s survey has found that, while 35 per cent of businesses had expected higher earnings in the September quarter, only 27 per cent delivered. Additionally, 19 per cent of firms experienced a decline in their profits compared to the 15 per cent that had initially forecast a drop in earnings. The Q1 2015 outlook for profits is 25.6 points, marginally higher than the 25.0 points forecast at the same time last year.

According to Gareth Jones, CEO of Dun & Bradstreet–Australia & New Zealand, despite a recent divergence between expectations and actual results, businesses are gradually improving their performance and optimism remains an important factor in future growth.

“Despite a backdrop of soft external conditions and macro-economic forces, business activity this year has been steady; with our survey revealing that most indicators are up on last year’s levels,” he said. “Optimism also remains strong, with 74 per cent of businesses reporting they are more optimistic about growth in the next 12 months compared to the last.

“Despite a backdrop of soft external conditions and macro-economic forces, business activity this year has been steady; with our survey revealing that most indicators are up on last year’s levels,” he said. “Optimism also remains strong, with 74 per cent of businesses reporting they are more optimistic about growth in the next 12 months compared to the last.

“The recent separation in expected and actual business performance, however, suggests that the business environment is, in reality, still weak. “If this trend continues, and given the persistent weakness in consumer confidence, there is a risk that this optimism will fade, and with it a willingness for businesses to invest, employ and drive more significant growth,” Mr Jones added.

D&B’s Business Expectations Survey reveals a further improvement in the three-month outlook from businesses, with expectations for capital investment, employment, selling prices and sales in the first quarter of 2015 moving ahead of last year’s levels, although profits expectations are flat year-on-year.

At 27.5 points the expected selling prices index for Q1 2015 has jumped to its highest level since 2009. Thirty-one per cent of firms indicate they will lift their prices at the start of the New Year, while just three per cent intend to discount and the remainder will leave their prices unchanged.

Employment expectations have edged up marginally to 14.8 points, with 23 per cent of businesses planning to take on more staff while eight per cent will cut numbers. Actual employment activity remained weak in the past quarter, with 21 per cent reporting to have hired staff while 15 per cent reduced their numbers.

Similarly, capital investment expectations have lifted slightly as 21 per cent of survey respondents indicate they will spend money on their operations in Q1 2015 compared to the six per cent which will reduce expenditure. This response has taken the index to 15.7 points, up from 7.2 points expected at the same time last year.

Finance does not appear to be an obstacle for investment plans, with only seven per cent of businesses reporting access to credit as an issue for their operations. The most commonly listed issue is cash flow (24 per cent) and the current level of the Australian Dollar (25 per cent); with wholesalers and manufacturers in particular identifying the currency’s value as most likely to influence their operations.

To read the full survey report click on this link: Sentiment outstrips results – DB Business Expectations Survey – Q1 2015

For further information contact:

Josh Maher, Manager, Communications & Corporate Affairs, +61 3 9828 3644 maherj@dnb.com.au

{kind=link}