The Saudi Credit Bureau (SIMAH) launched its wide educational program Amwalk 2 as one of its long financial literacy programs, through which it deals with fundamental issues that will help all segments of society to build their future and achieve their financial goals, reduce financial defaults and enhance the culture of savings, the foundations of investment and planning.

With Amwalk 2, SIMAH aims to shed more light on a number of issues related to the financial and credit aspects of individual consumers in an effort to raise the level of financial literacy among consumers and introduce them to the importance of financial planning to organize and manage their financial resources. Amwalk 2 also aims to enhance the essential roles of SIMAH, being the 1st licensed credit bureau in Saudi market, in helping consumers to assess their creditworthiness and guide them into optimal use of credit cards.

Through Amwalk 2, SIMAH is actively contributing to the preservation of consumers’ rights following the eight credit principles, which are neutrality, transparency, education and awareness, credit behavior, complaints, protection and confidentiality. It also seeks to stress the importance of a credit report in organizing and managing budgets, taking financing decisions and knowing financial obligations with credit donors.

Financial knowledge and literacy of consumers play an important role in their ability to make important financial decisions. In the aftermath of the global financial crisis, the policymakers worldwide expressed deep concern about the lack of financial knowledge and, as the recent research has suggested, lack of financial literacy amongst different population groups. Faced with a wide variety of available financial products and services today, both individuals and company management need to be able to make informed financial decisions. The quality of these decisions will greatly depend on the level of knowledge of the decision makers, including their financial literacy. It has been argued that financial literacy could be one of the key factors of economic growth, as decisions made by management directly affect the business, financial performance and, ultimately, overall economy It is that gap that Amwalk 2 works to bridge.

Financial knowledge and literacy of consumers play an important role in their ability to make important financial decisions. In the aftermath of the global financial crisis, the policymakers worldwide expressed deep concern about the lack of financial knowledge and, as the recent research has suggested, lack of financial literacy amongst different population groups. Faced with a wide variety of available financial products and services today, both individuals and company management need to be able to make informed financial decisions. The quality of these decisions will greatly depend on the level of knowledge of the decision makers, including their financial literacy. It has been argued that financial literacy could be one of the key factors of economic growth, as decisions made by management directly affect the business, financial performance and, ultimately, overall economy It is that gap that Amwalk 2 works to bridge.

The diversity of community’s needs coupled with varying consumption patterns often lead to uncontrolled spending. Therefore, the financial management cannot be created properly. Especially if it is associated with the consumption pattern by using credit card based, consumers often cannot control their spending. Bills come at the end of the month become swollen because of the application of the system of compound interest of the creditors. If there is high bill and the ability of consumers to pay decrease, it will cause bad credit.

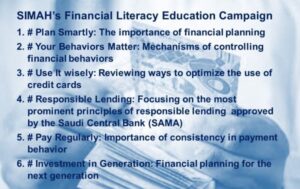

The first financial education campaign of Amwalk 2 was launched titled # Plan Smartly, in which SIMAH focused on educating individual consumers on the importance of financial planning through 5 main steps where the first step is to review the credit report to ensure financial commitments. As for the second step, it is to determine the monthly income and installments due, while the various goals come as the third financial steps, such as travel, marriage, buying a new car, etc. along with specifying the priorities of each one. As for the fourth financial steps, it is to develop a general financial plan and an estimated budget, while the fifth step focuses on a complete review of the plan after setting priorities.

The second campaign was under the title of # Your Behaviors Matter , which dealt in general with the mechanisms of controlling financial behaviors, predicting any emergency future conditions, and the importance of the consumer’s ability to differentiate between needs and desires and then drawing financial priorities on that basis, with the importance of saving and commitment to pay financial obligations.

The third campaign was titled # Use It wisely, which reviews ways to optimize the use of credit cards, and not to overuse them except when needed and in a smart way, while not buying with large sums of money that burden the consumer and may cause delay in paying credit card dues . Delay is just the beginning of defaulting.

As for the fourth campaign of Amwalk 2 , it came under the title # Responsible Lending , in which SIMAH focused on the most prominent principles of responsible lending approved by the Saudi Central Bank (SAMA). The principles aim to encourage responsible lending that meets the actual needs of consumers, especially those related to owning housing and assets rather than consumer purposes. The principles also aim to enhance financial inclusion by providing adequate financing for all segments of society, taking into account reasonable deductible ratios that the consumer can afford. In addition, the principles focus on ensuring fairness and competitiveness among creditors to make sure that their procedures and mechanisms are effective and efficient. The principles apply to all creditors and finance activities directed at consumers. These activities encompass all credit products and programs designed for individuals, including, but not limited to, personal finance, vehicle finance, credit cards and real estate finance. The creditor must set appropriate internal controls and procedures to ensure compliance with the principles herein, other relevant laws, regulations, and instructions. It must also pay special attention to documenting information and maintaining documents provided by consumers, thereby gaining an acceptable degree of reliability.

The creditor must assess the ability of its consumers to meet monthly credit obligations, especially in cases where consumer’s deductible ratios are close to the maximum deduction limits. The assessment of the ability to meet monthly credit obligations is primarily based on the assessment of the consumer’s monthly disposable income that can be used to meet his/her monthly credit obligations. Basic expenses that vary according to several factors, such as income levels, number of dependents, and residence place, whether the consumer owns such a place, rents it, or otherwise, must be taken into consideration, the creditor should develop appropriate rules in line with best practices to apply comprehensive factors to various categories of consumers. The finance is considered bearable if the consumer’s total monthly credit obligations, upon granting him/her finance, are less than the consumer’s monthly disposable income.

The fifth campaign came under the title # Pay Regularly, and with a new idea of depicting two characters who were embodied with almost the same circumstances with different credit behaviors. Nasser and Noura work in the same facility, earn the same salary, and live in the same city as well, but their credit behaviors are different. Noura is committed to repaying her financing loan while Nasser is lagging in repayment, sometimes by procrastination and sometimes by postponing until he became financially insolvent, and circumstances compelled him, due to his negligence and lack of commitment.

The sixth campaign came with a title of # Investment in Generation , in which Amwalk 2 reviews the most prominent feature of the financial habits that arise with the individual, and how those financial habits can positively or negatively affect the individual’s future behaviors, and the role of parents in helping their children to acquire the best financial habits, through behaviors such as saving, spending on the basics, not on luxuries, and simple investment methods that can root the importance of money for a child.

SIMAH intends to launch 25 financial education campaigns under the Amwalk 2 during the last two quarters of 2021. Participates with SIMAH in Amwalk 2 include Banking Awareness Committee , Saudi banks along with a number of SIMAH’s members.

“Amwalak 2 comes as an extension of Amwalk 1 that SIMAH launched in 2019, as one of the largest financial education programs. We really believe in the importance of spreading financial culture and we try to play a remarkable role in this aspect by highlighting consumers’ rights stipulated in the Credit Information Law (CIL) and its Implementing Regulations (IR), Code of Conduct and Consumer Awareness Procedural” says Swaied Alzahrani , SIMAH’s CEO.

He adds that consumers’ rights are among top priorities of SIMAH and we never interfere in our members’ decisions neither negatively or positively. “Financial education is progressively necessary, and not only for investors. it’s turning into essential for the typical family making an attempt to determine the way to balance its budget, buy a home, fund the children’s education and ensure an income when the parents retire. Consumers have forever been responsible for managing their own finances on each day to day basis – pay on a vacation or save some money for new furniture; what proportion to place aside for a child’s education or to line them up in life – however recent developments have created financial education more and more necessary for financial well-being” SIMAH’s CEO adds.

Alzahrani clarifies that SIMAH seeks to correct some misconceptions through the Amwalk 2, such as banning travel or blocking services, as SIMAH does not at all prevent government services or prevent any consumer from traveling, as its role is limited to collecting, preserving and exchanging credit information according to the CIL & its IR and under Saudi Central Bank (SAMA) supervision.

SIMAH big data, demographic information, financial and other variables available in credit reports help lenders to extrapolate the borrower’s credit behaviors based on complex mathematical models that use the variables and data of the credit report as key indispensable inputs to support lending decision and risk management. “ SIMAH, in the process of evaluating consumers’ creditworthiness and by providing credit reports, does not provide any opinion, decision and/or comment that would oblige any member to grant or deny any credit facilities. On this basis, SIMAH has, since its foundation, inserted the following statement in each credit report issued” Alzahrani elaborates.

SIMAH now plays an important role in helping consumers, corporates and SMEs obtain financing. SIMAH’s credit data on individuals and /or corporate borrowers provided to its members helps remove uncertainty that has traditionally been associated with lending.

SIMAH has issued more than 116 million credit reports to the Saudi market since its establishment in 2004 until the end of December 2020, which enabled SIMAH’s members to identify the credit behaviors of their customers without interfering with any of their negative or positive decisions. SIMAH works to provide an effective and reliable financial infrastructure to ensure sustainable economic growth increase the confidence between lenders and borrowers, reduce financial risks, and support monetary policies. Lenders’ abilities to price the cost of risk vary dynamically and according to the possibility of default of the borrower, which allows one of the most important tools of monetary policy, which is interest rates, to directly affect economic behavior, such as borrowing, investment and consumption rates. “SIMAH has significantly activated the role of the SIMAH Care since its development in 2018 and improved all its mechanisms, as the center was able to serve more than 847,577 beneficiaries during the period 2018-2020, while more than 169,315 thousand disputes were closed by the end of the fourth quarter of 2020” CEO of SIMAH illustrates .

SIMAH has been able, SIMATI & SIMAT (consumer and commercial reporting systems), to cover many major sectors in Saudi market. The size of SIMAH’s database of consumers since 2004 until the end of the fourth quarter of 2020 amounted to about 18 million consumers (individuals and companies), while the total number of scores provided by SIMAH during the period (2018-2020) amounted to more than 28 million credit scores. The total number of credit accounts in SIMAH reached about 71 million credit accounts, while the total transactions provided by SIMAH 360 reached more than 26 million transactions during the period (2018-2020).

For Full press release, click here

About SIMAH

![]() Founded in 2002 and started operation in 2004, Saudi Credit Bureau (SIMAH) is the first credit bureau in Saudi Arabia supervised , regulated and licensed by Saudi Central Bank (SAMA) to provide both consumer and commercial world class products and services. Innovativity of SIMAH stems from its robust ability to meet stakeholders’ needs in both government and private sectors. SIMAH’s marketing concept is FINDATA while more than 383 key data providers contribute big data to SIMATI & SIMAT ( SIMAH consumer & commercial reporting systems) . More than 116 million credit reports were issued by SIMAH since 2004 till end of 2020 while total number of credit instruments until end of 2020 was more than 71 million. Total number of consumers reports stored in SIMAH database is more than 18 million which explains Saudi Arabia Depth of Credit Information Index being 8 out of 8 in 2020.

Founded in 2002 and started operation in 2004, Saudi Credit Bureau (SIMAH) is the first credit bureau in Saudi Arabia supervised , regulated and licensed by Saudi Central Bank (SAMA) to provide both consumer and commercial world class products and services. Innovativity of SIMAH stems from its robust ability to meet stakeholders’ needs in both government and private sectors. SIMAH’s marketing concept is FINDATA while more than 383 key data providers contribute big data to SIMATI & SIMAT ( SIMAH consumer & commercial reporting systems) . More than 116 million credit reports were issued by SIMAH since 2004 till end of 2020 while total number of credit instruments until end of 2020 was more than 71 million. Total number of consumers reports stored in SIMAH database is more than 18 million which explains Saudi Arabia Depth of Credit Information Index being 8 out of 8 in 2020.

{kind=link}